Tariffs, PWC softness weigh on Yamaha profits despite stable motorcycle performance in 2025

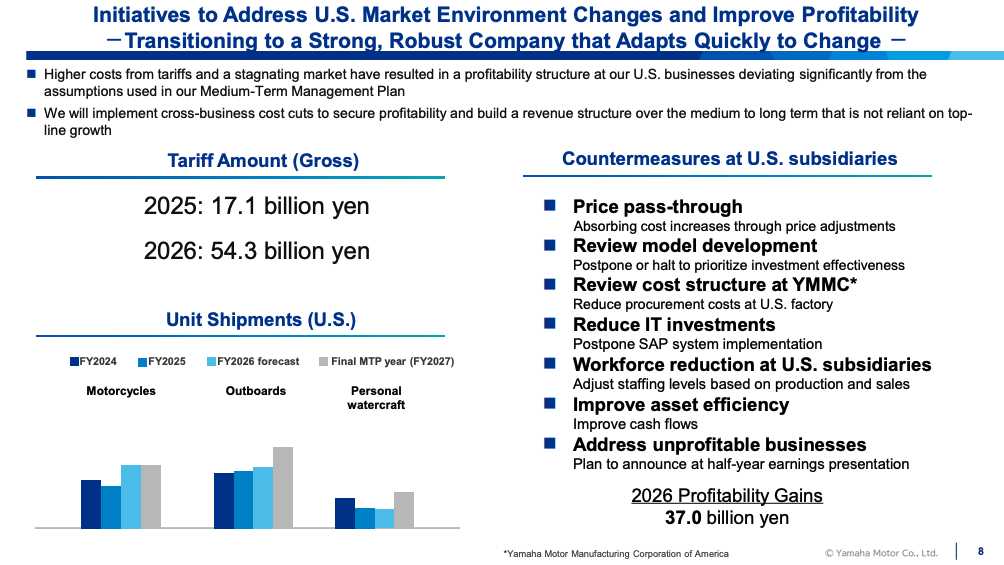

Yamaha Motor Co. reported a sharp decline in profitability for the fiscal year ended Dec. 31, 2025, as U.S. tariffs, higher costs and weakness in personal watercraft and side-by-side sales weighed on results.

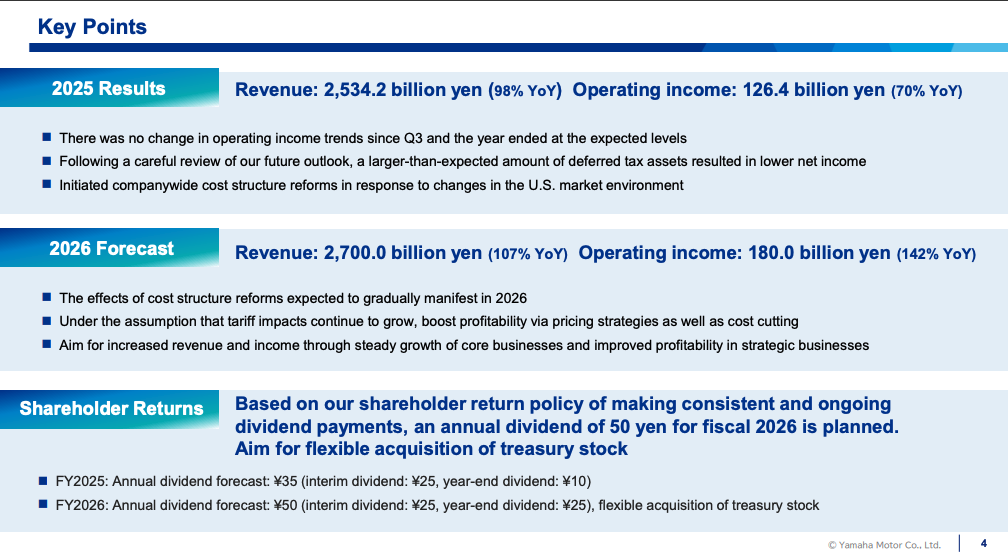

Revenue for the year totaled ¥2.53 trillion ($16.6 billion USD), down 1.6% year over year. Operating income fell 30.4% to ¥126.4 billion ($825 million), while net income attributable to owners of the parent dropped 85.1% to ¥16.1 billion ($105 million).

Yamaha Motor’s President and CEO Motofumi Shitara cited continued global uncertainty, including U.S. tariff policy and foreign exchange fluctuations, as key headwinds. Higher procurement costs, increased R&D and SG&A spending, and impairment losses in the company’s Outdoor Land Vehicle (OLV), i.e., ORV, business further pressured margins.

Motorcycle business stable

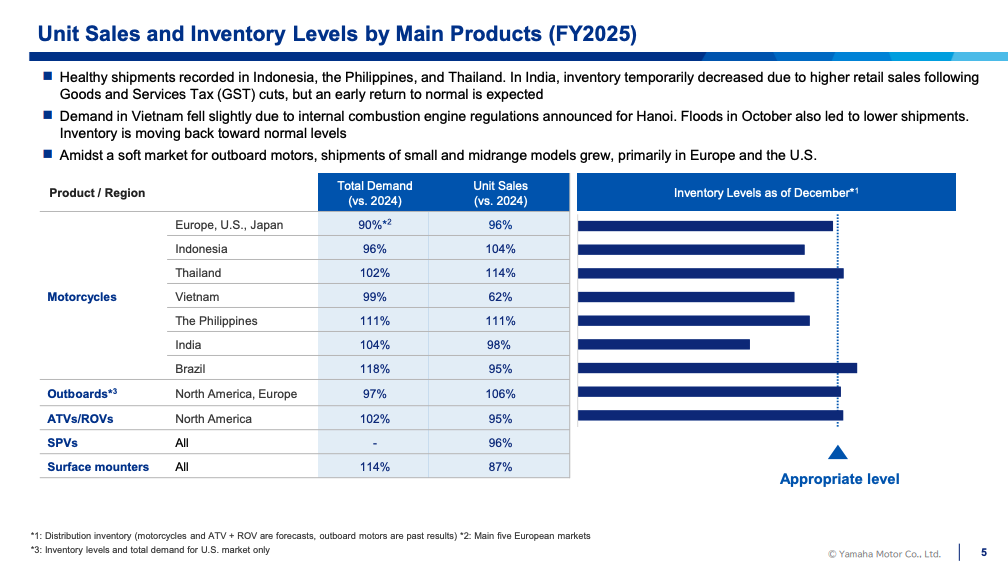

Yamaha’s Land Mobility segment — which includes motorcycles — generated ¥1.62 trillion ($10.6 billion) in revenue, essentially flat year over year. Operating income in the segment increased 4.6% to ¥108.7 billion ($710 million).

Unit sales increased in Indonesia, the Philippines and Thailand, while demand in Europe and the U.S. softened slightly. Production and shipment suspensions in Vietnam also weighed on volume.

Although revenue remained stable, the company says higher procurement costs, tariff impacts and increased expenses limited margin expansion.

Marine segment hit by U.S. PWC slowdown

In Yamaha’s Marine segment, revenue declined 1.9% to ¥527.6 billion ($3.45 billion), while operating income dropped 39% to ¥53.6 billion ($350 million).

Demand for outboard motors in the U.S. — Yamaha’s primary market — remained roughly in line with the prior year. However, personal watercraft demand declined in the U.S., contributing to lower overall marine revenue and profitability.

Higher R&D spending, increased labor costs and the continued impact of U.S. tariffs compounded the decline in segment earnings.

OLV losses widen

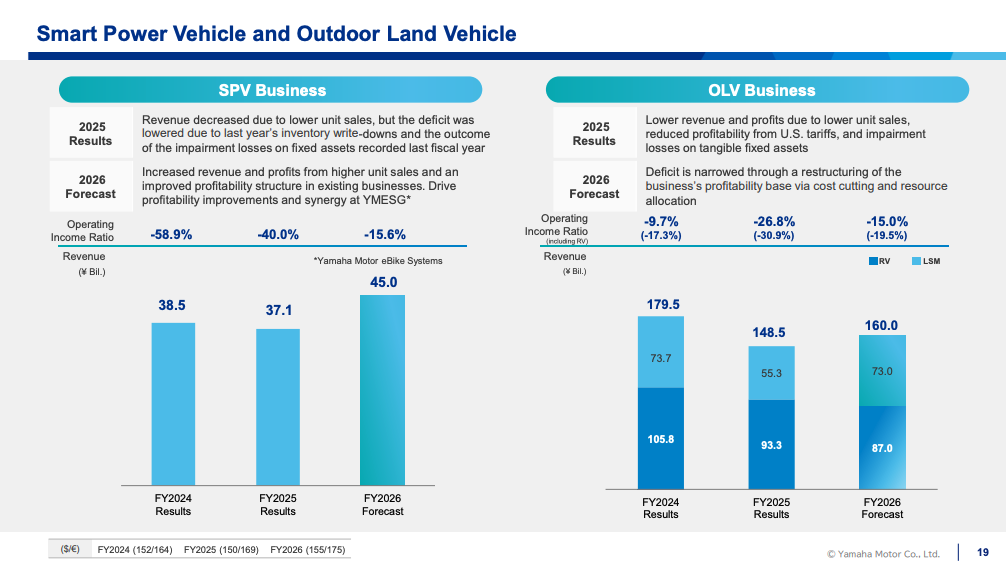

Yamaha’s Outdoor Land Vehicle segment (ORV) — which includes ATVs, side-by-sides and low-speed mobility vehicles — was the company’s largest profitability drag.

Revenue fell 17.2% to ¥148.5 billion ($970 million), and the segment posted an operating loss of ¥39.8 billion, widening from a ¥17.4 billion ($260 million) loss the previous year.

While ATV sales were described as strong, lower ROV sales, tariff impacts and impairment losses on tangible fixed assets drove the decline. The low-speed mobility business, including golf cars, also experienced weaker demand in the U.S.

Inventory management matters

Both Polaris and BRP worked to reduce excess network stock, which has helped stabilize dealer turnover and protect margin. Yamaha’s broader OLV weakness, combined with inventory impairment charges, suggests dealers may have faced slower turns and promotional pressure.

2026 outlook calls for rebound

Despite continued tariff exposure, Yamaha is forecasting higher revenue and profits in fiscal 2026.

The company expects stronger motorcycle unit sales in emerging markets and growth in outboard motors. In strategic businesses — including Robotics, Smart Power Vehicles and OLV — Yamaha projects improved profitability due to structural reforms and the absence of impairment losses recorded in 2025.

For U.S. powersports dealers, the results underscore continued tariff-related margin pressure and softness in the personal watercraft and side-by-side categories, even as Yamaha’s core motorcycle business remains resilient globally.