Maximizing F&I profits through reinsurance

This article originally appeared in the September edition of Powersports Business and was written by Brad Stanek and Paulina Matel.

It is no secret that these are challenging times for powersports dealers. The Fed’s high interest rate policy has raised floor plan costs and curtailments for dealers. It has raised gas prices and inflation for consumers, including your customers. Meanwhile, the historically low unemployment rate means you must pay more than ever to attract and retain good employees. These factors are clearly depressing dealership valuations. But despite these headwinds, there are still plenty of opportunities for savvy dealers. Take reinsurance, one of the most overlooked and often misunderstood strategies for dealership growth and wealth accumulation.

What is reinsurance?

Reinsurance is a strategy in which dealerships participate in the underwriting profit of the F&I products they sell such as service contracts, limited warranties, and ancillary products.

Instead of paying premiums to an insurance company, the dealer pays premiums to an insurance entity that they own – an entity with a favorable tax structure and creditor protection. Dealers like F&I products because historically they have low loss ratios (i.e., a low percentage of customers making claims). The dealer (rather than a third party insurance company) gets to pocket the difference between claims paid out and premiums received. This surplus can build up over time in the reinsurance account and can turn into a very nice future retirement nest egg for the dealer.

Just know this strategy can be complex and you do not want to be a do-it-yourselfer here.

Reinsurance specialist, Scott Miller, partner at Safe Harbor Advisory Partners, said on a recent webinar that dealers often tell him, “I keep hearing about reinsurance, but I don’t understand it.” Or, “I heard about another dealer who did reinsurance, and it didn’t work out so well.” That is often a red flag, according to Miller. “If reinsurance did not work out for a dealer, you must go back and look at where the money came from to fund the company and what kind of structure the F&I department started out with. If you are going to go the reinsurance route, make sure you do it right,” he adds.

Benefits of reinsurance

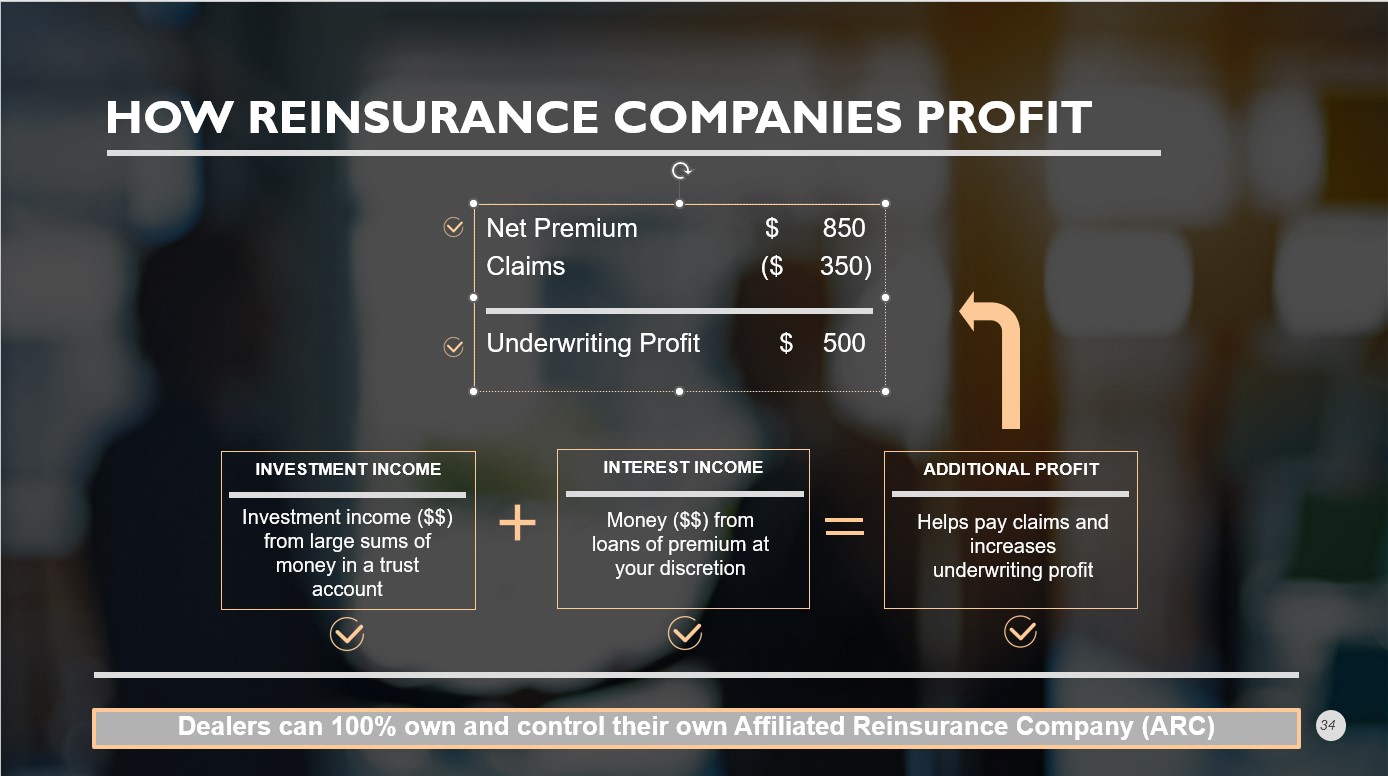

A reinsurance company is designed to create underwriting profit. The net premium, which sits in the bank account, can be invested by a financial advisor. In addition to the potential for investment income, there is potential interest income. For instance, if a dealer took a loan out against the available cash assets of the insurance company, they would pay themselves back with premium and with interest at the applicable federal rate. That interest goes back into the dealer’s account and adds additional profit to the trust account.

Let’s say you sold a five-year extended service contract or a tire and wheel contract. The gross premium is what you remit to the service contract company after administrative fees are deducted from the net premium. It is the money that goes into the reinsurance company trust account. After the contract is earned, any claims that were paid for things like mechanical breakdown, tire and wheel damage, or a gap claim, are netted out. Any net premium that is left is the underwriting profit (i.e., Net Premium – Claims = Underwriting Profit).

Miller says to go into reinsurance with the following mindset, “Every time I deliver a bike/unit, I activated the following profit centers. If you control the finance and you sell two products every time you deliver, you have three additional profit centers every time you deliver a bike or unit. You can silo those profit centers and measure your performance from there.”

Advantages of reinsurance

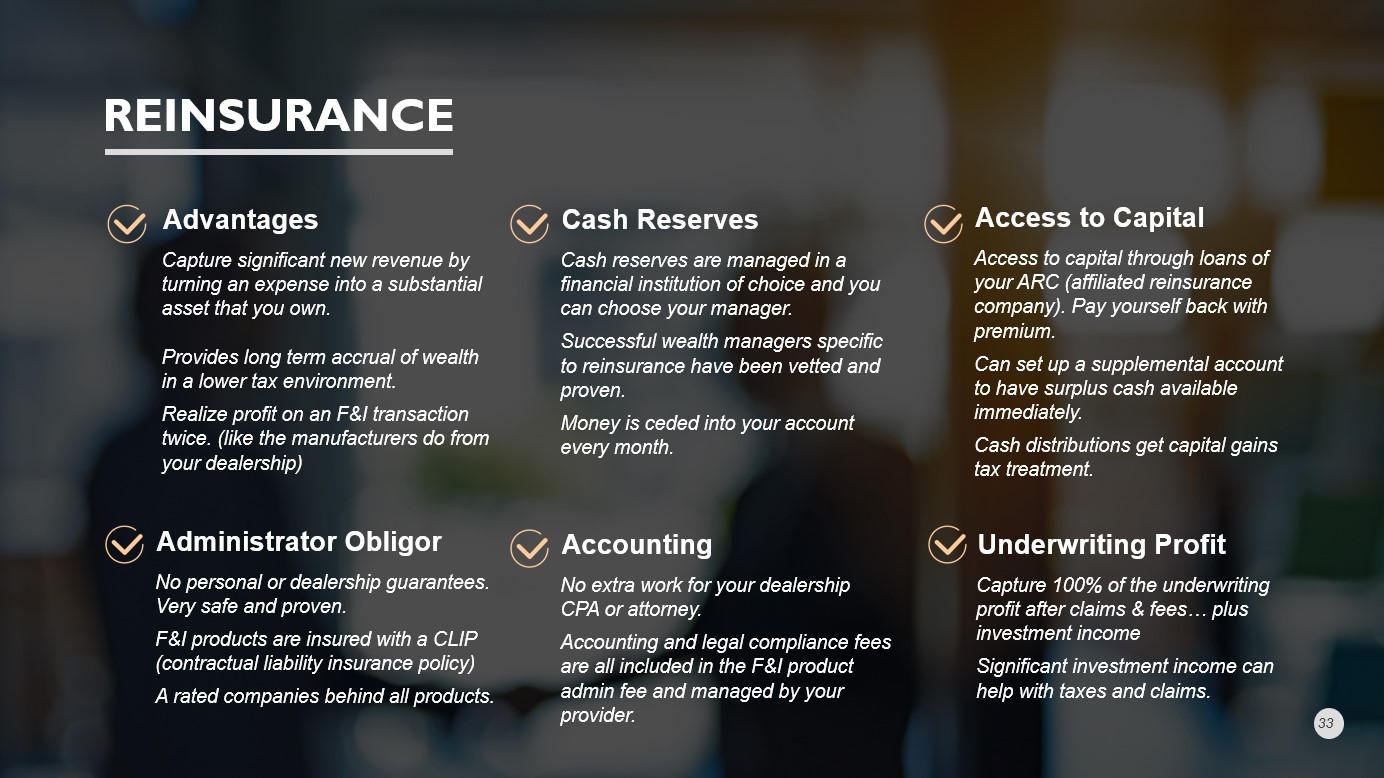

Most of you have an operating company (your dealership). Many of you also have a real estate company since you own the land and/or facility on which your dealership sits. And you have your own personal wealth. When you do reinsurance, you are forming and owning a third company. According to Miller, this is what allows you to turn a percentage of the premium you are earning on your F&I products and limited warranties into an asset. As the cash reserves build up, Miller says you can access it to fund the growth of your dealership.

“The big advantage of reinsurance is administrator obligor,” Miller says, which means you (the dealer) and your dealership transfer most of the risk to the administrative company that then places insurance on it. “Every contract that you sell (i.e., service contract, limited warranty, etc.) has a CLIP (Contractual Liability Insurance Policy) that is underwritten by a major insurance company, but you still participate in 100% of the underwriting profit” Miller says.

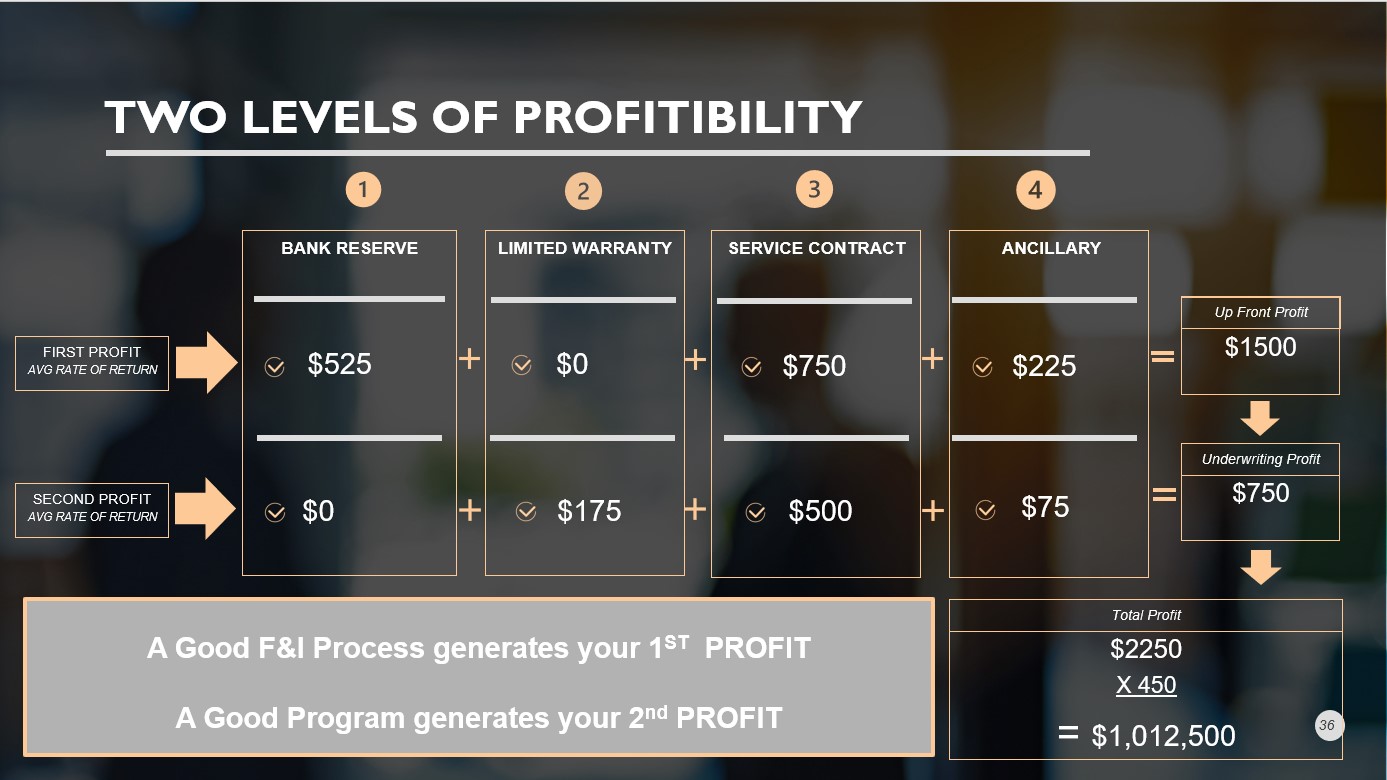

“Let’s say you deliver a motorcycle and make a $1,500 profit on the F&I transaction. It does not have to end there. If you captured net premium on multiple products and seed that in your reinsurance company, you could generate another $750 in underwriting profit through your reinsurance company on that one transaction alone,” Miller says. “Now you are at $2,250 in profit. Let us say you do 450 transactions per year. That is more than $1 million in additional profit.”

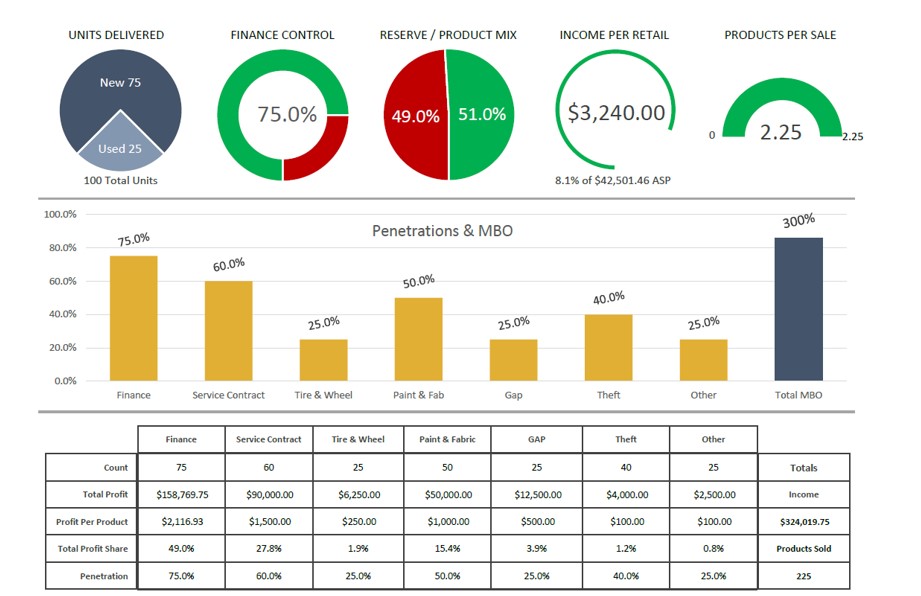

“When you own a reinsurance company, you can see a monthly ‘session statement’ report that includes a balance sheet, P&L and bank statements, and a breakdown of how each model and trim number is performing,” he continues. “The premium that you put in is going to create a loss ratio. For instance, if $1,000 in premium goes into the reinsurance entity and there are $500 in claims, then your loss ratio is 50%, which is in the midrange.”

According to Miller, you must sit down and look at the products you are selling and how the quality of the products affects your ability to reinsure the money you are underwriting in your F&I department. “Some [bikes] will have lower loss ratios than others, just like some of the F&I products will have lower loss ratios than others,” Miller says. “Once you have the right formula you can say with confidence: ‘With this product lineup and this F&I suite, we can expect a loss ratio of X.’ If the sales forecast comes true and the F&I penetration is what you expect, you can say with a high degree of certainty, ‘this is how much money we’re going to seed into our reinsurance position this year,’” says Miller.

Over time, he explains that you can start to project what those numbers will look like over five to ten years. “Reinsurance can become a very substantial wealth asset if you’re willing to commit to it, but it’s not something you try for only a year or two,” he says. “It takes three or four years to finetune the process and gauge what your run-loss ratios will be for your dealership or dealerships.”

Your main operating company (your dealership) is subject to lots of economic volatility. The F&I can help smooth out that volatility. Miller says this is why a reinsurance strategy should be implemented at least five to ten years before you make a major ownership transition. “It takes some time for the underlying contracts to earn out.”

Reinsurance as a growth engine

According to Miller, your F&I department, with a solid reinsurance foundation “is your catalyst for growth.” To grow your dealership, you will need more inventory. To sell more inventory, you will need more salespeople. Good salespeople are expensive to hire. To keep those people busy, you will need to have more people walking through your door and that means you must spend more on advertising and marketing. All that costs money. “Your sales department may turn a profit of 5 percent to 15 percent,” says Miller. “Your service department and parts department may each generate a profit of 5 percent to 10 percent. That is not enough surplus cash to plow into growth.”

“By contrast, a good F&I department returns 80 percent to the bottom line as opposed to traditional margins of 5 percent to 15 percent on sales, service, and parts,” he continues. “This is what generates the capital to grow the dealership. This is what allows you to invest in more inventory, more salespeople, and more marketing and advertising to get more customers in the door.” Like Miller, I have found that a strong reinsurance program contributes greatly to dealership valuation.

Reinsurance as wealth strategy

You have to work incredibly hard to build your business. Reinsurance is one part of the total wealth puzzle. As a member of the National Powersports Dealer Association, you are entitled to a complimentary Second Opinion Service (i.e., Total Wealth Analysis) about your businesses at no cost and no obligation. If you’re trying to determine whether it makes sense to have a reinsurance entity based on how many units you sell, how many contracts you sell, and what you might get as a net profit over the next five to ten years, then we can give you specific numbers as part of our complimentary service.

Every owner has different goals with respect to what they want to accomplish with their dealership, and what they want for themselves and their family post-exit. Before taking any transition steps it is important to know how much money you will need to accomplish your goals.

Importance of a written plan

To determine this, you will need a formal written plan to determine not only if reinsurance makes sense for you, but if you are getting a fair return on your other liquid investments (cash, stocks, bonds, mutual funds, annuities, etc.). Further, you will want to be sure your tax pro is really helping you mitigate taxes – not just processing your tax return every year. You will also want to ensure you have no gaps in your insurance coverages, and that your wealth is protected in the event you get sued, divorced, or victimized by cybercrime.

Finally, if you are planning to exit your business, do you know what its true value is? It may not be as much as you think. Do you know what you need to do to maximize its value before exiting? Have you taken the steps to make sure your family is adequately protected if you die or become disabled unexpectedly?

Conclusion

Again, our complimentary Second Opinion Service can help you identify gaps in your plan and give you a specific list of actions to take to do what’s best for you, your family, and your team. You have worked too hard to build your business. Do not leave anything to chance.

Brad Stanek is a financial advisor, executive director, and financial wealth planner of in Chicago, IL brad.stanek@ms.com. Paulina Matel is a financial advisor in Chicago, IL paulina.matel@ms.com.