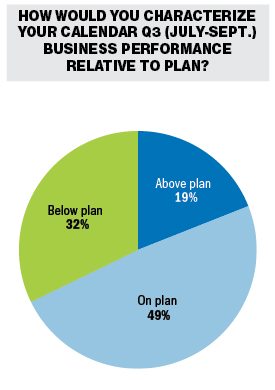

Majority of dealers reach plan for Q3

Increased sales for SxS and motorcycles

Despite the majority reporting “somewhat weak” overall business conditions, 68 percent of dealers said their performance was on or above plan, based on results of the Q3 2015 Powersports Business/RBC Capital Markets Dealer Survey. A total of 121 dealers from 41 states and three Canadian provinces completed the survey.

The states not represented are Alabama, Alaska, Georgia, New Hampshire, New Jersey, Ohio, Oregon, Rhode Island and Wyoming. Dealers from those states who are interested in participating in the fourth quarter survey should send an email to PSB Editor in Chief Dave McMahon at dmcmahon@powersportsbusiness.com and request to be added to the list.

Overall, the responding dealerships sell more than 47 brands of motorcycles, ATVs, side-by-sides, snowmobiles and PWC. A total of 109 of the 141 respondents (90 percent) are single-store owners.

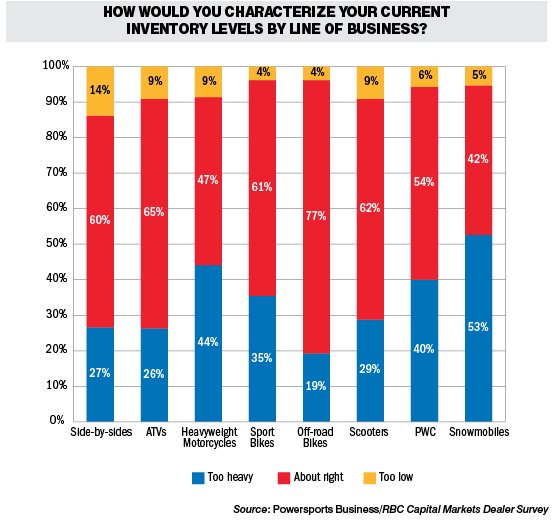

Side-by-sides

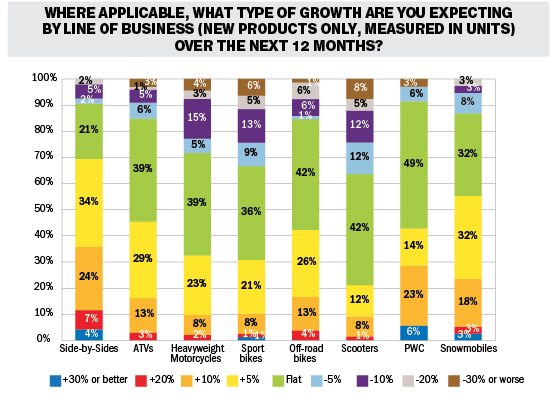

RBC Capital Markets analyst Joe Spak reported that side-by-side industry retail growth grew mid-single digits (4-6) percent in Q3. “Industry wide, dealer next twelve month (NTM) expectations look similar vs. our 2Q15 survey and are generally optimistic,” Spak said. “By brand, Polaris dealers appear just as optimistic as 2Q15, though many have noted discounting cutting into dealer profits.”

With the addition of the new Can-Am Defender launching BRP into the utility side-by-side segment, it’s no surprise that dealer expectations are more positive for that brand as well. “Can-Am (BRP) dealer expectations appear to be have improved, which we partially attribute to the new utility side-by-side category,” Spak said. Yamaha and Honda expectations were consistently strong, as Spak noted how the release of the Honda Pioneer 1000 and Yamaha YXZ1000R sport side-by-side have improved those dealers’ outlook into the fourth quarter.

“Industry side-by-side inventory levels look improved versus earlier this year and roughly a similar inventory sentiment versus 3Q14,” he added.

Motorcycle

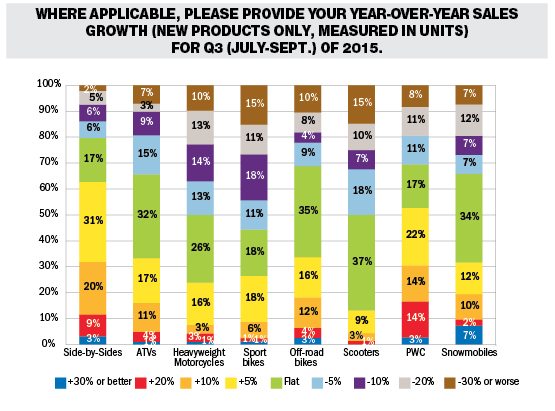

Of the dealers surveyed, 53 percent reported their motorcycle segment business performance was on plan, while 20 percent were above plan. “It does appear that 3Q15 Harley-Davidson retail sales growth improved,” said Spak, who put Q3 retail sales at an increase of 2-3 percent year-over-year.

On a brand perspective, Harley-Davidson increased despite low investor expectations, though increased shipments could mean heavy inventory for Q4.

“Polaris’ Indian brand looks very strong, while Victory looks a little slower than 2Q15. Can-Am (Spyder) expectations [are] still OK, but we are picking up a slightly downward trend perhaps as Spyder enthusiasm runs out a bit,” Spak said.

As far as inventory, the majority of dealers noted that in they still believe inventory levels are too high. “Harley inventory declines appear to have been offset by increases across some other brands,” Spak said.

ATVs

In the ATV segment, 67 percent of those surveyed said they were on or above their current business performance plan. Despite softer sales in this quarter, ATV inventory levels remained steady.

“Looking ahead, dealer industry optimism looks more muted vs. 2Q15,” Spak said. “The same is the case (to varying degrees) by brand with the exception of Polaris where optimism looks to be trending up. This may be in part driven by new product introductions.”

Snowmobiles

When separated by product segment, snowmobiles reported the highest percentage on or above plan with 78 percent. Forty-three percent of snowmobile dealers said that customer buying interest is somewhat better, which is the highest percentage since 2014.

Spak said that snowmobiles appeared soft in Q3, though it is still early within the season for growth. Dealer expectations for the next twelve months was reported as optimistic, with 50 percent predicting a 5-10 percent increase in retail sales.

Next Twelve Months

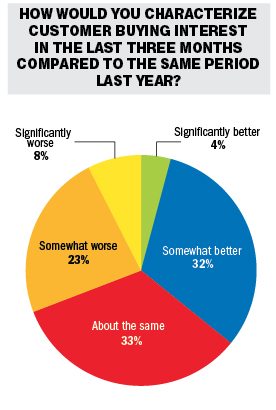

Customer traffic increased in Q3, with a large number of dealers saying it was somewhat better or significantly better than Q2. Fifty-three percent of dealers said customer buying interested remained the same year-over-year.

Overall, interest by product remained consistent with the previous quarter in side-by-side, ATV and motorcycle segments. As far as the dealer’s next twelve months (NTM) view, Spak said that “heavyweight motorcycles and ATVs also ticked lower as weak sales environment continues to drag. Side-by-side expectations are more flattish, but we note [they] have remained fairly optimistic.”

WINNING DEALERS

The following dealers who completed the Q3 2015 Powersports Business/RBC Capital Markets Dealer Survey each were selected at random to win a $100 Best Buy gift card, courtesy of RBC Capital Markets.

Jan Downing, Outdoors in Motion, Rutland, VT

Raymond Walters, Got Gear Motorsports, Ridgeland, MS

Tony Cozzone, Team Carolina Powersports, Lancaster, SC

Lonnie Apol, Apol’s Harley-Davidson, Alexandria, MN

Mike Goff, Snake River Yamaha, Meridian, ID

All dealers who complete the survey receive a PDF analysis of the results from RBC Capital Markets and are eligible for the $100 Best Buy gift card.