Analyst provides BRP fiscal Q2 expectations ahead of earnings call

BMO Capital Markets analyst Gerrick Johnson has provided Powersports Business with a research note prior to BRP reporting its Q2 fiscal year 2021 results on Thursday.

Following is Johnson’s report:

“BRP (DOO) reports 2Q21 financial results tomorrow before the open. We expect DOO to report normalized loss per share of ($0.35), down from normalized EPS of $0.71 in the year ago period. We are below the Street consensus estimate ($0.23). Like most leisure companies in our coverage, we expect production shutdowns early in the quarter to weigh on results. However, demand for the company’s products has remained strong, and we therefore expect positive management commentary.

“Key Points

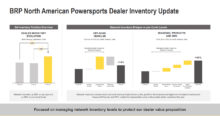

“For 2Q21, we expect revenue to decline -39% to $890 million, below the Street consensus of $953 million (-35%). We expect DOO to report normalized EBITDA of $59 million, compared to $168 million in 2Q20. The Street consensus is $74 million.

“We expect Year-Round Products to generate revenue of $451 million (-39%).

“We expect revenue from Off-Road Vehicles to decline -40% to $366 million. We think BRP’s ORV retail sales increased +60% in the quarter.

We expect Spyder Roadster sales of $85 million, down -32% year over year.

We expect Seasonal Products revenue of $272 million (-37%)

“We estimate PWC revenue declined -40% yoy to $192 million and snowmobile sales declined -26% to $80 million. We think DOO’s 2Q20 PWC retail sales increased +20%, with lack of dealer inventory being a limiting factor.

“We expect revenue in the marine segment to decline -48% to $64 million, with the late May announcement of the discontinuation of Evinrude being an incremental headwind.

“We estimate boat and Marine PAC sales to decline -38% and -16%, respectively.

“We expect Powersports PAC & OEM Engine revenue to be $103 million (-41%).

“We expect gross margin will contract 620 bps year over year to 16.3% from 22.5% owing to loss of sales leverage and high sales allowances. The Street consensus calls for 570 bps of gross margin contraction to 16.8%.

“Given the uncertainty around the COVID-19 pandemic, DOO did not issue formal FY2021 guidance, though it did indicate it expects 2H21 sales to decline -10% to -20%.

“We currently expect FY2021 EPS of $1.45 on sales of $4.88 billion, while the Street is expecting EPS of $2.10 on sales of $5.18 billion.”